Chapter 47 — Effectiveness of Policy Options to Meet All Macroeconomic Objectives

Cambridge International AS & A Level Economics (9708) · Unit 10.3 · 4th edition coursebook

Learning objectives

- Evaluate the effectiveness of fiscal policy including Laffer curve analysis in relation to different macroeconomic objectives.

- Evaluate the effectiveness of monetary policy in relation to different macroeconomic objectives.

- Evaluate the effectiveness of supply-side policy in relation to different macroeconomic objectives.

- Evaluate the effectiveness of exchange rate policy in relation to different macroeconomic objectives.

- Evaluate the effectiveness of international trade policy in relation to different macroeconomic objectives.

- Analyse problems and conflicts arising from the outcome of the different policies.

- Explain the existence of government failure in macroeconomic policies.

Key terms

- crowding out

- the idea that higher public sector spending will just replace private sector spending.

- crowding in

- the idea that higher public sector spending will increase private sector spending.

- Laffer curve

- a curve showing tax revenue rising at first as the tax rate is increasing and then falling beyond a certain rate.

- government macroeconomic failure

- government intervention reducing rather than increasing economic performance.

- counter-cyclically

- going against the fluctuations in economic activity.

47.1The effectiveness of fiscal policy in relation to different macroeconomic objectives

Fiscal policy is rarely able to deliver every macroeconomic objective at once. The discussion below sets out the main reasons why.

Economic growth and low unemployment versus balance of payments stability and price stability

Expansionary fiscal policy raises aggregate demand. It can therefore increase actual economic growth and reduce cyclical unemployment. The same higher demand can, however, pull up the price level (demand-pull inflation) and worsen the current account of the balance of payments. Contractionary fiscal policy faces the mirror-image problem: lower aggregate demand can help bring inflation down and improve the current account, but at the cost of higher cyclical unemployment and slower actual growth.

Crowding out and crowding in

There is a long-running debate over whether higher government spending always raises aggregate demand. New classical economists argue that higher government spending financed by increased borrowing draws funds away from private-sector lending and pushes up the rate of interest. The smaller pool of funds and the higher cost of borrowing reduce consumption and private-sector investment. On this view, public-sector spending crowds out private-sector spending. The higher interest rate can also attract foreign financial investment, push up the exchange rate and reduce net exports.

Keynesians reject the crowding-out story. They argue that crowding in occurs instead: higher government spending raises GDP by a multiple amount through the multiplier; the resulting higher income increases saving, which provides the funds for new lending; and higher income also raises consumption and investment. On this view, public-sector spending can pull private-sector spending up alongside it.

Unexpected responses

There is no certainty as to how households and firms will respond to fiscal changes. A cut in income tax and corporate tax rates may not raise consumption and investment if households and firms expect that the cuts will soon be reversed and so save the windfall instead of spending it.

Time lags

Fiscal policy is subject to long time lags. By the time a government recognises a recession, decides on a policy tool, gets the change through legislation and waits for households and firms to react, the economy may already be entering a boom. Expansionary policy then arrives once the negative output gap has closed and a positive output gap is opening, adding to inflationary pressure rather than offsetting the recession.

Difficulties of reversing an increase in government spending

Some forms of government spending carry a long-term commitment that cannot easily be reversed. Building more state-run hospitals, for example, locks in staff and equipment costs for decades, even when the economy is booming. The alternative — closing facilities later — typically carries considerable political unpopularity.

Redistribution of income and development versus the incentive to work

Fiscal policy is the main tool for redistributing income and supporting development. Progressive taxes and transfer payments move money from the rich to those on low incomes, and government spending on state healthcare and state education raises life expectancy and educational performance for low-income groups. The risk is that higher transfer payments reduce the incentive for the unemployed to seek work. If that happens, the unemployed and their children may experience greater long-run poverty than if they had taken a low-paid job — because being in employment itself builds skills and improves the chance of a higher-paid job later.

The Laffer curve

The Laffer curve (see Figure 47.4) shows that when tax rates are already high, raising them further can be counterproductive. It was first drawn by the US economist Arthur Laffer in the early 1970s as adviser to President Ronald Reagan, to support the view that a cut in tax rates may actually raise tax revenue by stimulating both real economic activity (through stronger incentives) and declared economic activity (less tax evasion). At a tax rate of 0% there is no revenue, and at 100% there is also no revenue because workers will not work if everything is taxed away. Somewhere in between is a revenue-maximising rate. Pushing the rate beyond that point reduces revenue, because it discourages effort and encourages evasion. The curve therefore suggests that, apart from the maximum point, any given level of revenue can be raised at two different tax rates — a low one and a high one.

Economists question the usefulness and validity of the Laffer curve. The shape of the actual relationship is debatable: it may be linear over part of its length, and any shape is likely to vary between countries and over time. Empirical evidence also suggests that belief in the Laffer curve can lead to government failure: soon after the curve was shown to Ronald Reagan, the US government introduced tax cuts that actually reduced tax revenue rather than raising it.

Key concept link — The role of government and the issues of equality and equity

Changes in fiscal policy can have an impact on equality and equity. For instance, a rise in indirect taxation is likely to fall more heavily on people on low incomes and some may consider this to be unfair.

When government borrowing pushes up interest rates and discourages private investment, the rise in public spending displaces, rather than adds to, private spending. This is the classic definition of crowding out. Automatic stabilisers, the accelerator and the substitution effect describe different mechanisms — only crowding out captures higher borrowing leading to less private investment via higher rates.

Greater income equality requires deliberately reshaping the income distribution through progressive taxes and targeted transfer payments — these are fiscal tools. Trade, monetary and supply-side policy can affect efficiency, growth or stability, but they cannot directly transfer income between households the way taxation and benefits can. So fiscal policy is the most effective lever for redistribution.

A minimum wage set below the market wage has no bite — firms already pay above it, so it neither raises low-wage earnings nor narrows the income gap. Progressive taxes, benefits to low-income households and removing sales tax on food consumed by the poor all genuinely transfer resources towards lower earners. Hence a sub-market minimum wage is the least effective redistributive tool.

47.2The effectiveness of monetary policy in relation to different macroeconomic objectives

Monetary policy is also unable to deliver every objective at once. The reasons overlap with fiscal policy but include some that are specific to the way monetary policy operates.

Economic growth and low unemployment versus balance of payments stability and price stability

Expansionary monetary policy can support economic growth and reduce unemployment, but the same easier monetary conditions can raise demand-pull inflation and worsen the current account.

Time lag

Both fiscal and monetary policy operate with a time lag, but monetary policy tends to have a shorter lag because it is faster to change the rate of interest than to design, legislate and implement changes in taxes and government spending.

How commercial banks respond

Monetary policy reaches households and firms through the commercial banking system. If the central bank raises the interest rate it charges commercial banks, those banks may not pass the rise on to customers if they think that keeping lending volumes up will generate more profit. Quantitative easing — the central bank buying financial assets from commercial banks in return for cash — increases banks' liquid assets and their capacity to lend, but there is no guarantee that they will do so. If commercial banks are pessimistic about the future, they may be reluctant to lend, worried about borrowers' ability to repay.

Liquidity trap

Quantitative easing has typically been used when interest rates are already very low. A further cut in an already-low interest rate may have little impact: the economy is in a liquidity trap.

Influence of changes in other countries

A central bank's freedom to choose its interest rate is limited by what other central banks are doing. If a central bank wants to raise its interest rate to discourage borrowing, but other central banks cut theirs or hold them low, domestic firms can simply borrow from abroad. Foreign savers may also move money into the country's commercial banks to capture the higher interest rate, which expands the assets of those banks and their lending capacity — undoing some of the original tightening.

Unexpected responses

As with fiscal policy, household and firm reactions are not always predictable. In optimistic times, a higher interest rate may not be enough to discourage consumption and investment.

Demand and supply-side shocks

Both fiscal and monetary policy depend on officials being able to assess current performance and forecast private-sector activity accurately. Both can be thrown off course by demand- or supply-side shocks. A central bank may raise interest rates a year in advance of an expected boom; if a global recession then occurs while the rate rise is taking effect, the country may end up with a deeper recession than it would otherwise have had.

Mobility of financial investment

With financial capital increasingly mobile across borders, it is hard to maintain an interest rate noticeably different from rival countries. A rate cut below rival rates can trigger an outflow of hot money. A rate rise can discourage foreign direct investment, because it raises the cost of borrowing for foreign firms operating in the country and signals that demand there may slow.

Co-ordination

Monetary and fiscal policy need to be co-ordinated. A government push for growth can fail if the central bank simultaneously raises the interest rate.

Key concept link — Time

Time lags can have a significant impact on all the main forms of government policy.

Lower interest rates work by making borrowing cheaper, encouraging consumption and investment. But the demand boost depends on how much of any extra income households actually spend — the marginal propensity to consume. If the MPC is falling, households save more of any extra disposable income, so the multiplier shrinks and the rate cut has less impact on growth.

47.3The effectiveness of supply-side policy in relation to different macroeconomic objectives

Supply-side policy measures fall into two groups: market-based measures and interventionist measures.

Market-based supply-side policy

Market-based supply-side tools work by widening the role of market forces. They include cuts in direct tax, cuts in unemployment benefit, privatisation, deregulation and labour market reforms. Cuts in direct tax and in unemployment benefit aim to raise aggregate supply by strengthening the incentives to work and to be entrepreneurial. Privatisation, deregulation and labour-market reforms aim to raise aggregate supply by widening competition and reducing the costs of complying with government rules and regulations.

Market-based supply-side policy may raise economic growth and reduce inflation, but it can conflict with the objectives of redistribution of income and low unemployment, and it may even reduce growth rather than increase it. Cuts in income tax and unemployment benefit tend to transfer money from the poor to the rich, not the other way round. Privatisation has made some buyers of state-owned industries very wealthy; in pursuit of profit, some privatised firms have raised prices and so taken a higher share of the income of low-income groups. Labour-market reforms that reduce the power of trade unions, and deregulation that removes a national minimum wage, can also lower the relative pay of those on low incomes.

Cuts in income tax and unemployment benefit widen the gap between paid employment and transfer payments, but they do not necessarily raise employment and growth. Job vacancies may not exist; the unemployed may lack the skills and qualifications to fill the vacancies that do exist; or the vacancies may be in different areas of the country from where the unemployed live. Cuts in income tax may have unintended consequences as well: rather than working more hours, some workers may prefer to maintain their current disposable income and take more leisure time. Privatisation may not automatically raise efficiency and lower costs: a state-owned industry may be sold off as a monopoly, or sold as several firms which later merge into one. Deregulation can have similar effects, and removing health-and-safety rules can damage workers' health and cause accidents, both of which reduce productivity and growth.

Interventionist supply-side policy

Interventionist supply-side policy involves a larger role for government. Its main tools are government spending on education, training, infrastructure and support for technological improvement. Education and training take time to have an effect, but if they succeed they have the potential to improve every macroeconomic objective: they can raise both actual and potential growth, lower inflation, improve the current account, reduce unemployment, support development and reduce income inequality.

The qualifications still apply. Education and training may be in areas that turn out not to be in demand, and workers may not take up training opportunities. Improvements in infrastructure and technology can also have side-effects: building more roads and airports can create more air and noise pollution and so harm development, and advances in technology can cause structural unemployment as old jobs disappear.

Key concept link — Efficiency and inefficiency

Supply-side policy measures are designed to increase efficiency. However, there may be times when the use of certain policy tools may increase inefficiency. For example, firms given a subsidy to develop new production methods may become complacent.

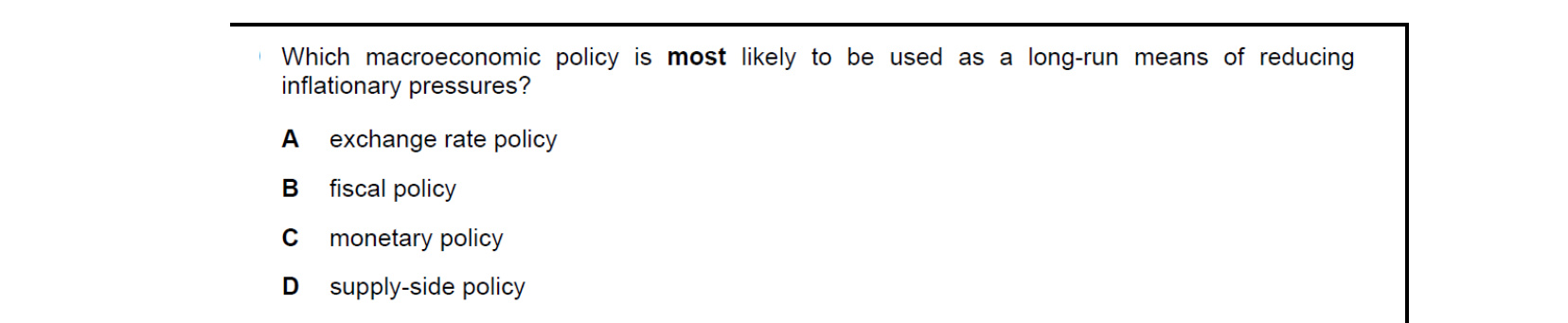

Inflation can stem from demand pressures or from supply-side weaknesses. Exchange rate, fiscal and monetary policy mainly squeeze aggregate demand and tend to lower output as well — costly long-run tools. Supply-side policy (education, deregulation, training, competition) raises productive capacity, allowing the economy to grow without overheating, so it is the preferred long-run anti-inflation policy.

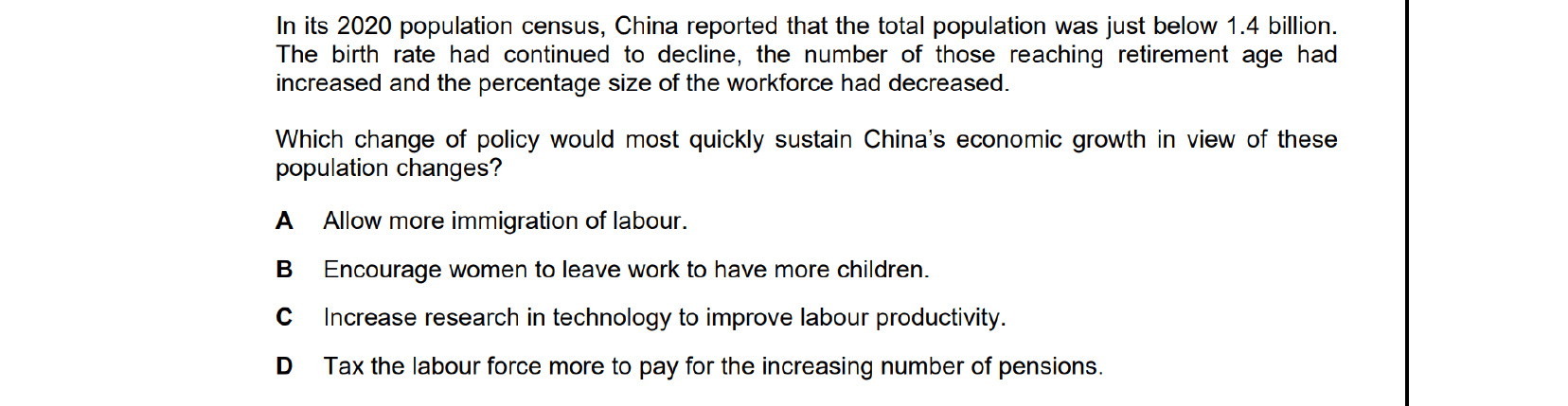

With a falling workforce share and an ageing population, China needs more workers fast. Encouraging immigration of labour adds workers directly and almost immediately, sustaining output and growth. Encouraging women to leave work shrinks the workforce; researching technology takes years to raise productivity; and taxing labour more discourages work. So the quickest fix is to allow more immigration of labour.

47.4The effectiveness of exchange rate policy in relation to different macroeconomic objectives

As with the other policies, there are reasons why exchange rate policy may not be successful in achieving all the macroeconomic objectives. The exchange rate works through the prices of exports and imports in foreign and domestic currency, and changes in those prices then ripple through the current account, aggregate demand and the price level. Whether the policy delivers improvements depends on the responsiveness of trade flows, the behaviour of speculators, and the reactions of other countries and central banks.

Balance of payments stability, economic growth and low unemployment versus price stability

A government can lower the exchange rate to improve the current account of the balance of payments, raise economic growth and reduce unemployment. A lower exchange rate makes exports cheaper in foreign currency, which may increase the quantity demanded of exports and so raise export revenue. It also makes imports more expensive in domestic currency, which may lower demand for imports and reduce import expenditure. Higher net exports raise aggregate demand, and this can increase output and create more jobs.

However, a lower exchange rate may also cause cost-push inflation and demand-pull inflation. The price of imported raw materials and capital goods rises, pushing up firms' costs of production; at the same time, the competitive pressure on domestic firms to restrain rises in their costs is weakened because foreign substitutes are now dearer. The rise in net exports raises aggregate demand, which can result in demand-pull inflation if the economy is approaching full employment. There is therefore a clear tension between using a lower exchange rate to support the external balance, growth and jobs, and the goal of price stability.

To reduce inflation, a government may instead seek to raise the exchange rate. A higher exchange rate produces higher export prices and lower import prices. This has the potential to reduce aggregate demand (through lower net exports) and to lower the costs of production. It may, however, increase a deficit on the current account of the balance of payments, reduce economic growth and increase unemployment. There are several factors that limit how effective exchange rate policy can be in either direction.

Price elasticity of demand

The effect of changes in the price of exports on export revenue, and of changes in the price of imports on import expenditure, depends on the price elasticity of demand. If demand for exports is elastic, a fall in the price of exports causes export revenue to rise; if demand for exports is inelastic, the same price fall reduces export revenue. The same logic applies to imports. For a depreciation to improve the current account, the sum of the price elasticities of demand for exports and imports must in practice exceed one — if not, the depreciation will worsen the deficit, at least in the short run, because the fall in price outweighs the rise in quantity.

Speculation

Under a floating exchange rate system, a government may instruct a central bank to sell the country's currency to bring about a depreciation. However, if there is strong speculation that the currency will rise in value, private-sector purchases of the currency may exceed the central bank's sales, and the exchange rate will move in the opposite direction to the one the policy intended. Expectations of speculators can therefore overpower official intervention.

Objectives of other countries

The governments of other countries may object to a government seeking to lower its exchange rate if they think it is doing so to gain an unfair competitive advantage for its products. This can lead to retaliatory exchange-rate or trade measures. The rise in the price of imported raw materials and capital goods may, in any case, soon erode any competitive advantage gained by feeding into higher domestic costs and prices.

Availability of foreign currency

A central bank may want to raise the exchange rate if inflationary pressure is building up. Its ability to do this may be restricted by a lack of foreign currency reserves with which to purchase its own currency. Without sufficient reserves the central bank cannot sustain the higher rate, especially against persistent selling pressure.

Actions of other central banks

A country's exchange rate is also influenced by the actions of the central banks of other countries. For example, one central bank may sell its currency to buy a foreign currency in a bid to reduce the value of its own currency. If, however, the foreign central bank does not want this to occur, it can buy the first country's currency, offsetting the intended move. The exchange rate is a relative price between two currencies, so the policies and actions of partner central banks are part of the constraints on what any single central bank can achieve.

It is also important to remember that exchange rate policy is not only used to influence the balance of payments. Changes in a country's exchange rate can influence economic growth, unemployment and inflation, so any assessment of its effectiveness has to consider its impact on all four macroeconomic objectives together rather than judge it against the external balance alone.

47.5The effectiveness of international trade policy in relation to different macroeconomic objectives

A government can promote free international trade by removing restrictions on imports and exports. Free trade can raise economic growth by allowing the country to take greater advantage of comparative advantage. A free-trade policy is more likely to succeed if other governments adopt the same approach.

Some governments instead favour trade protectionism. Protection can help safeguard employment in particular industries, support infant industries until they reach efficient scale, and discourage dumping. The success of protection is limited by several factors. Firms can become dependent on protection and lose the incentive to improve. Other governments may retaliate, leading to a trade war. Membership of a trade bloc may simply prevent a government from imposing restrictions on other members of the bloc.

Key concept link — Progress and development

If industries do take advantage of any protection given to them, they may help a country's economic progress. However, there is a risk that protectionism may encourage inefficiency and reduce economic progress.

47.6The problems arising from conflicts between policy objectives

The choice of policy tools is shaped by the risk that achieving one objective makes another harder to achieve. The main conflicts run as follows.

Low unemployment and economic growth versus price stability

Expansionary fiscal and monetary policy tools used to reduce unemployment or raise the growth rate can raise inflation. Contractionary tools used to reduce demand-pull inflation can in turn slow growth and raise unemployment. A government may try to side-step this trade-off by adding supply-side policy tools, which in the long run can lower both inflation and unemployment and raise the growth rate.

Low inflation versus balance of payments stability

A conflict can also arise between low inflation and a smaller current account deficit. If a central bank raises the rate of interest to cool inflation, the higher rate is likely to cause an appreciation of the currency. The stronger exchange rate may worsen the current account position even as it attracts hot money flows on the financial account, and the higher interest rate may also raise unemployment.

Redistribution of income versus economic growth

There can be a conflict between greater income equality and faster economic growth. Making income tax more progressive and raising benefits for low-income groups may discourage effort and enterprise, and may reduce foreign direct investment. The conflict is not absolute. Raising the living standards of the poor may improve the health and education of part of the labour force, which raises productivity. Effort and enterprise may also be driven more by wage rates and profit levels than by tax rates, and foreign direct investment can still be attracted by rising domestic demand and an increasingly skilled workforce even when tax rates are relatively high.

Number of policy tools

To avoid these conflicts, a government can use a separate policy tool for each objective: cutting income tax to lower unemployment, for instance, while devaluing the currency to improve the current account. In practice, governments use a combination of fiscal, monetary and supply-side policy tools together.

47.7Government failure in macroeconomic policies

Government macroeconomic failure occurs when macroeconomic policy measures cause a deterioration, rather than an improvement, in economic performance. Several recurring reasons explain why it happens.

Miscalculating the size of the multiplier

If a government understates the size of the multiplier, it may increase its spending by too much and end up swapping one problem — a negative output gap — for another — a positive output gap.

Time lags

Many policy tools work through a sequence of time lags: a recognition lag before the government sees that inflationary pressure is building; an implementation lag while the policy tool (such as a rise in income tax) is drawn up and introduced; and a behavioural lag before the policy actually changes how households and firms behave. By the time the policy tool bites, the economy may have moved on, making the policy inappropriate. As a result, fiscal and monetary policy used to offset the business cycle sometimes end up reinforcing it rather than working counter-cyclically. There is also no guarantee that the response will be in the expected direction. During a boom, a higher interest rate is meant to encourage saving and discourage borrowing, but optimistic households and firms may continue to borrow and spend.

Desire to win elections

Elected governments may be tempted to introduce popular but economically questionable policy tools ahead of elections. Measures such as a rise in government spending on pensions may win votes without necessarily improving macroeconomic performance.

Pressure groups and corruption

Policy tools can also be shaped by powerful pressure groups, and there is the further risk of corruption among officials. The textbook records that past attempts to reduce class sizes and increase resources in education and improve healthcare in Honduras were hindered by corrupt government officials who stole money from government budgets.

Key concept link — Efficiency and inefficiency

The key concept of efficiency is clearly linked to government failure. When a government implements a policy tool, it is seeking to improve economic efficiency but, as explained in this chapter, there are a number of reasons why the tools may worsen rather than improve the economy's performance.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

The Laffer curve plots tax revenue against the tax rate. At very low rates, raising the rate lifts revenue; but beyond an optimal point, higher rates discourage work, encourage avoidance and shrink the tax base, so revenue falls. The curve therefore illustrates that, as the tax rate increases, tax revenue will eventually fall — not rise indefinitely.

Redistribution from rich to poor takes income from high earners (potentially blunting incentives to work, save and invest) and gives it to lower earners. This trade-off — narrower income gaps at some cost to economic efficiency — is only worthwhile when society places greater weight on equality than on efficiency. So policy B is most appropriate when equality is valued more highly than efficiency.

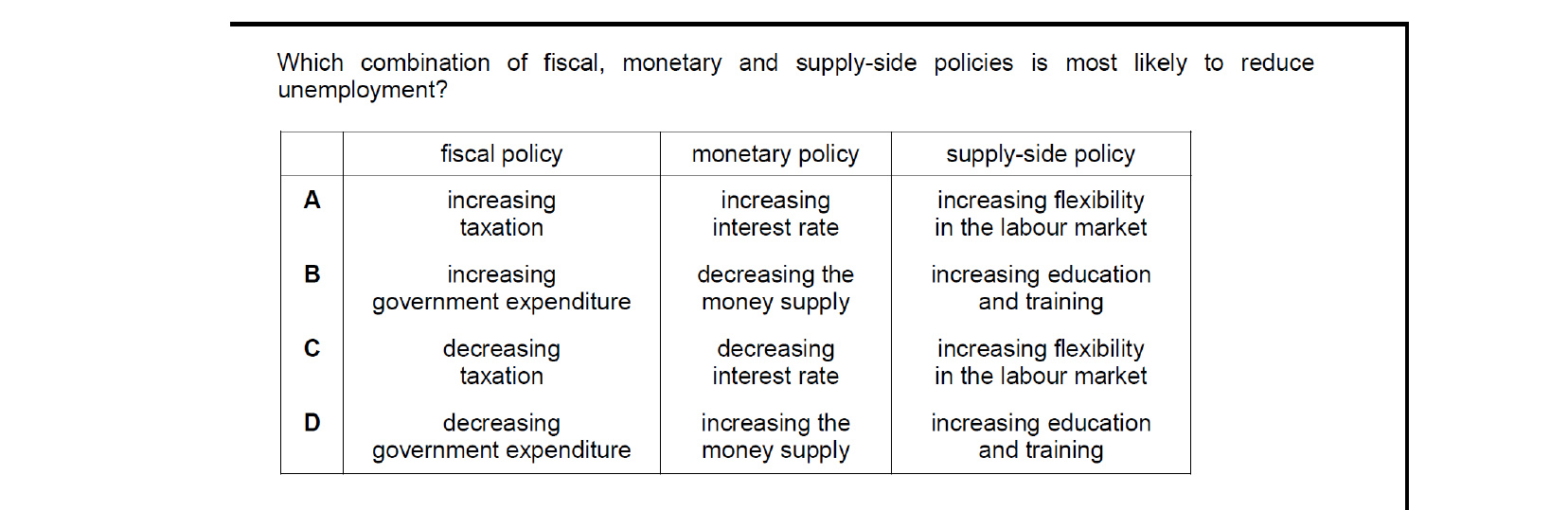

To reduce unemployment, all three policy levers must boost aggregate demand or improve labour-market flexibility. Cutting taxes raises disposable income and consumption (expansionary fiscal); cutting interest rates encourages borrowing, investment and consumption (expansionary monetary); and greater labour-market flexibility lets firms hire and reallocate workers more readily. Combination C — tax cuts, rate cuts and a more flexible labour market — pulls in the same direction.

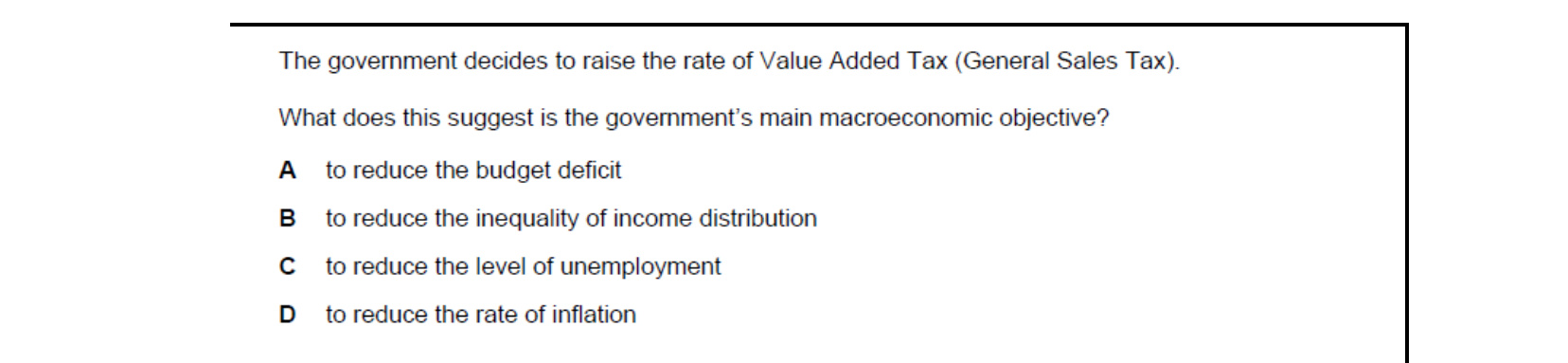

Raising VAT (a broad indirect tax) widens the tax base and pulls in extra revenue, directly shrinking the gap between government spending and tax receipts. So the move signals that the chief aim is to reduce the budget deficit. VAT is actually regressive (worsens inequality), reduces consumption (raising unemployment) and pushes the price level up — so it cannot be aimed at the other three objectives.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Evaluate the influence of crowding out or crowding in, how households respond, time lags and demand and supply-side shocks on the effectiveness of fiscal policy.

- Understand that the Laffer curve suggests that tax cuts may actually increase a government's tax revenue.

- Evaluate the influence of time lags, how commercial banks at home and abroad and how households and firms react and demand and supply-side shocks on the effectiveness of monetary policy.

- Understand that supply-side policy tools may be market-based or interventionist.

- Examine the impact of supply-side policy tools on the distribution of income, unemployment, competition.

- Examine the factors that limit the effectiveness of exchange rate policy.

- Examine the factors that may influence the effectiveness of international trade policy: promotion of free trade, trade protectionism.

- Analyse problems arising from conflicts between policy objectives.

- Discuss the reasons for government macroeconomic failure: lack of accurate information, time lags, unexpected responses, pressure groups, corruption.

Want more practice? Drill this chapter's past-paper MCQs (95 questions) →